Last month we talked to you about debt and how you can manage it to improve your credit score. Now let’s take a deeper look at credit.

Last month we talked to you about debt and how you can manage it to improve your credit score. Now let’s take a deeper look at credit.

Credit overview

Credit is a contract where a borrower owes money to a lender. These can be things like a mortgage, car note, student loan, or credit card. What likely comes to mind when thinking of credit is the credit score or ranking.

Credit Score Basics

A credit score is a measurement system where lenders can determine how risky it is to loan you money based on how well you are managing your money and paying your debts on time. The score ranges from 300 to 850, and the higher the number the more likely you are to get approved for a loan at the most favorable interest rate.

There are several things the scoring agencies take into account when calculating your credit score:

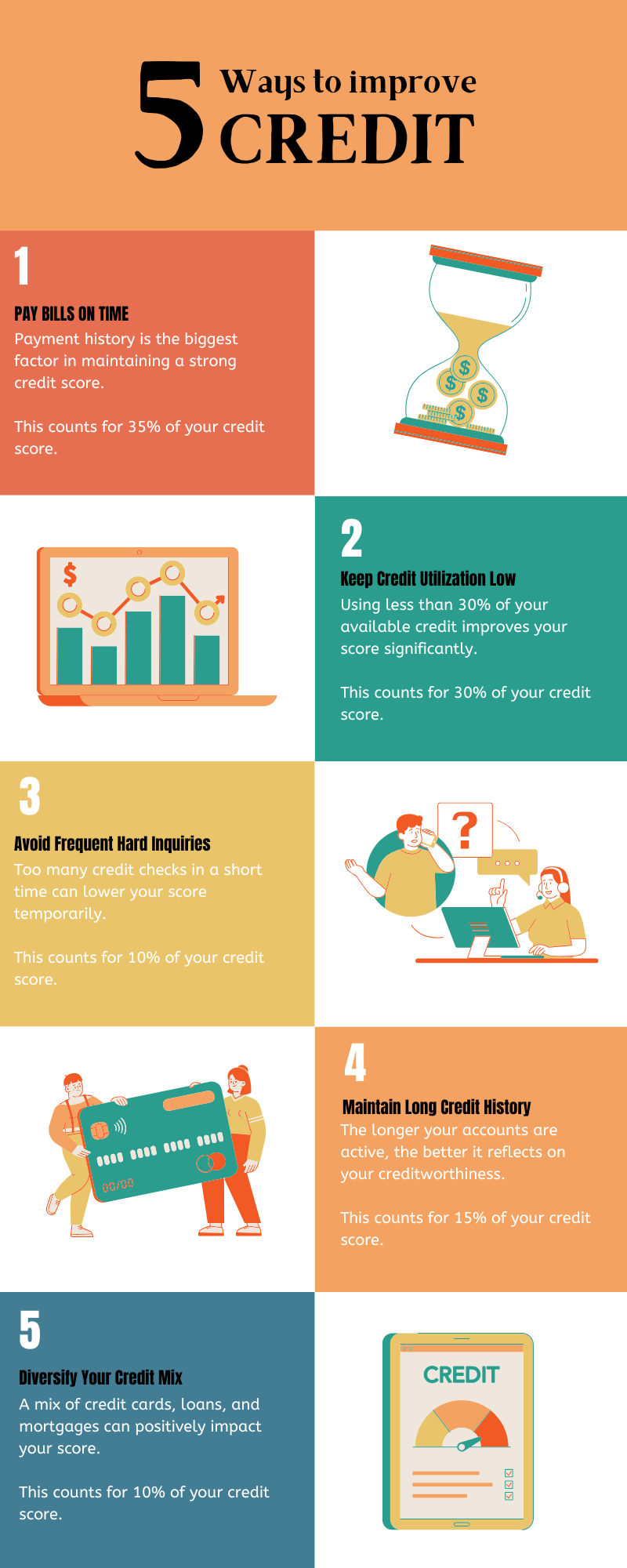

- 35% of your score is determined by your payment history (whether you pay your bills on time).

- 30% takes into account how much of the credit you have available that you are using. Basically, the less you are spending on your credit maximum, the better.

- 15% is based on how long you have had credit. So a 30-year-old who has had a credit card and paid it faithfully for 10 years will have a higher score than an 18-year-old with a credit card they have been paying for a few months.

- 10% is determined by your recently opened credits and inquiries. Every time you apply for a new line of credit (i.e. credit card), a lender will run an inquiry on your credit history. This will stay on your report for two years. At NeighborWorks Columbus we will run an initial credit history with a “soft inquiry” meaning it will not affect your credit score.

- 10% is from the types and mix of credit, meaning that its more favorable to have a variety of credit, like student loans, a car payment, and a mortgage. Of course, this is a low indicator in terms of affecting your score, so it’s far more important to be a good manager of your money than to take out multiple loans.

While it’s not necessary to memorize all the details of how your credit score is calculated, these give you a good idea of areas to work on if you are aiming to improve your credit score.

Since most of your credit score is determined by your money management, budgeting and tracking your spending is the best place to start. Here’s an article with some tips.

Next, you want to work on paying off debt and lowering your DTI, which you can read about here.

If you fall in the boat of being good at managing your money, but you have limited credit history established, this is the time to consider getting a credit card. You will want to use it cautiously and wisely and pay it off on time or else it will have a negative impact on your overall score.

All this information comes from the Freddie Mac CreditSmart Essentials program, which we are working through on our Third Thursday classes. If you’d like to join us, please sign up here.