Debt is something nearly every American has on some level, but how does debt really impact your ability to purchase a home? Let’s dive in.

Debt 101

Debt 101

Debt is anything you owe to someone else, including a car payment, student loans, credit cards, and more. Debt is often looked upon as negative, but if managed properly debt can be a tool to help boost your credit scores.

Not all debt is created equally. If you owe your Grandma $10, this does nothing for your credit score. If you have a small credit card that you use responsibly and pay off faithfully, that will raise your credit. On the other hand, if you are in over your head on payments or have too much debt, this will hurt your credit score and lending prospects.

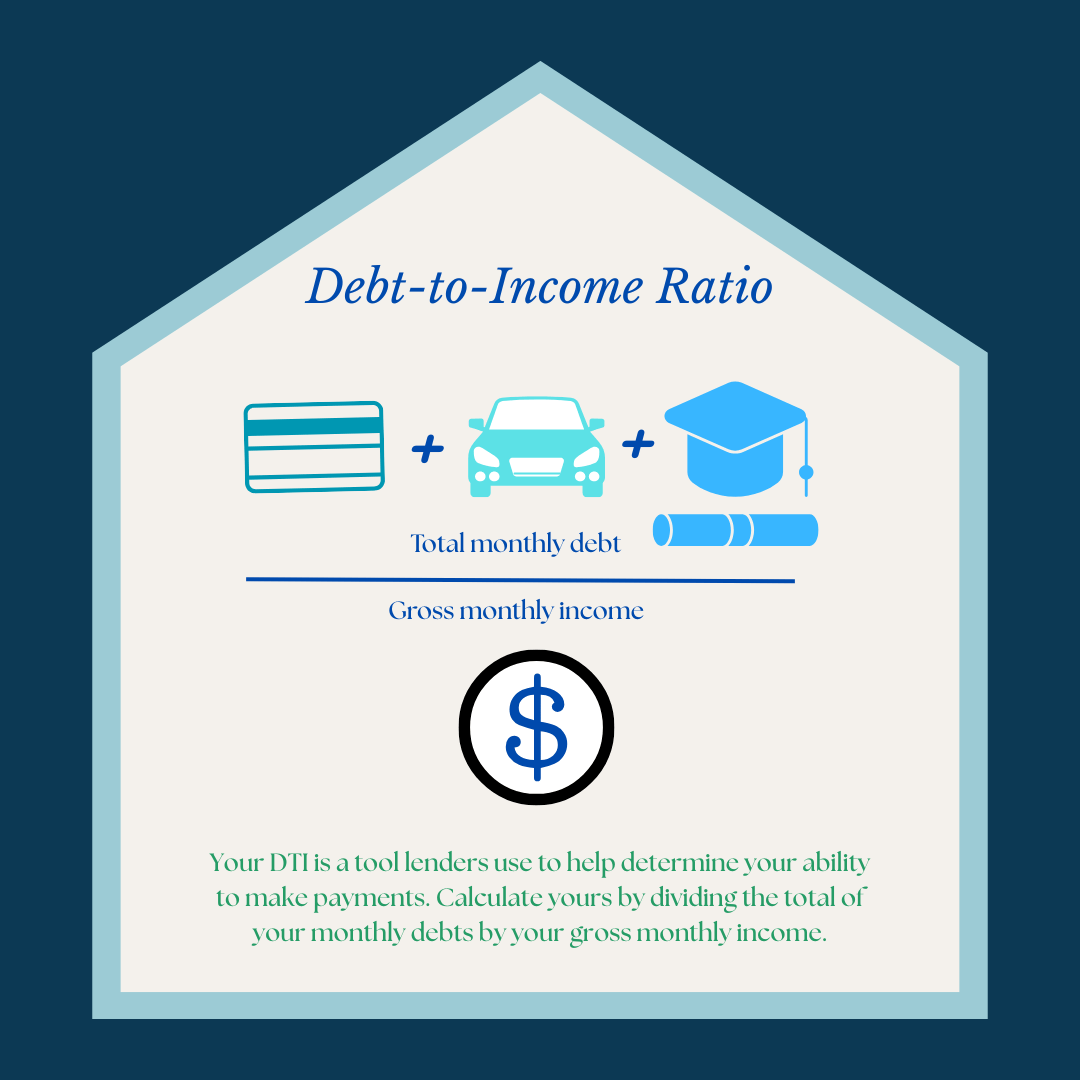

How much is too much?

That really depends. First, if you are not able to keep up with your payments, then you have too much debt.

The more technical answer comes down to your debt-to-income (DTI) ratio. This takes into account how much debt you have compared to your actual income. While it’s best to always keep your DTI as low as possible, to get approved for a mortgage, you need it to be 36% or lower.

To figure out this number for yourself, you add up all your recurring monthly debt amounts and divide them by your monthly gross income. So if you pay $25/month on your credit card, $100 on student loans, and $700 in rent, your monthly debt total is $825. Say you make $2,500/month in gross income. This would make your DTI 33%.

Wells Fargo has a handy DTI calculator here.

Can you change your DTI?

Yes, you can! In fact, this is one of the big things many of NeighborWorks Columbus’s clients work on in our Homeownership Program. Freddie Mac CreditSmart Essentials has several tips we will share on how you can start this process.

- Debt snowball

The debt snowball method is a popular strategy for reducing debt. You list all your debts by their total amounts, and make minimum payments on all of them except the smallest one. That one you pay all that you can toward it to pay it off first, then once that smallest one is paid, you begin on the next one and so on. This helps increase your spending power and boost confidence as you make progress on your goals.

- Debt avalanche

This method is similar in concept only instead of choosing the loan with the smallest dollar amount to start with you begin tackling the loan with the highest interest rate first. The pro of this method is you will pay less interest over time.

- Debt consolidation

Sometimes the best strategy is to consolidate your debt payments into one. You may be able to get better interest rates when you do this, and another advantage is it makes your life a little easier to only have one bill to manage.

This debt discussion is just the tip of the iceberg. In our Third Thursday Financial Fitness courses, we’re working through the Freddie Mac CreditSmart Essentials workbook for the next couple of months. Our next session is on Thursday, Aug. 21. Sign up here.

And, in our homeownership program, we work one-on-one with you to help you tailor these tips to your specific need. Begin your journey here.